The need for long-term care is generally defined by an individual’s inability to perform the

normal activities of daily living (ADL) such as bathing, dressing, eating, toileting, continence, and moving around. Conditions such as AIDS, spinal cord or head injuries, stroke, mental illness, Alzheimer’s disease or other forms of dementia, or physical weakness and frailty due to advancing age can all result in the need for long-term care.

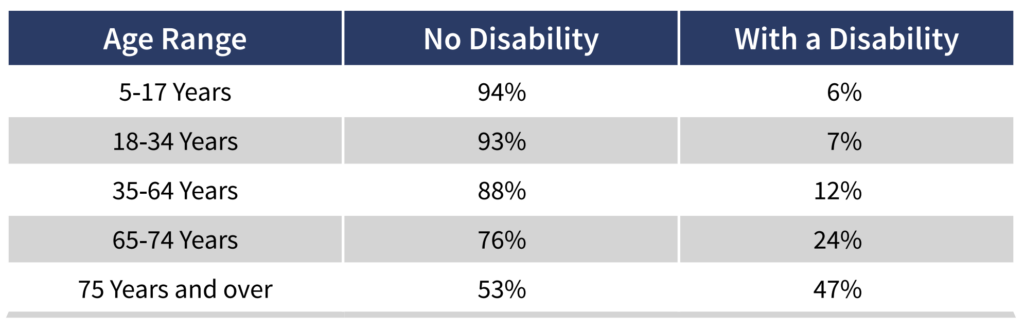

While the need for long-term care can occur at any age, older individuals are the typical recipients of such care.

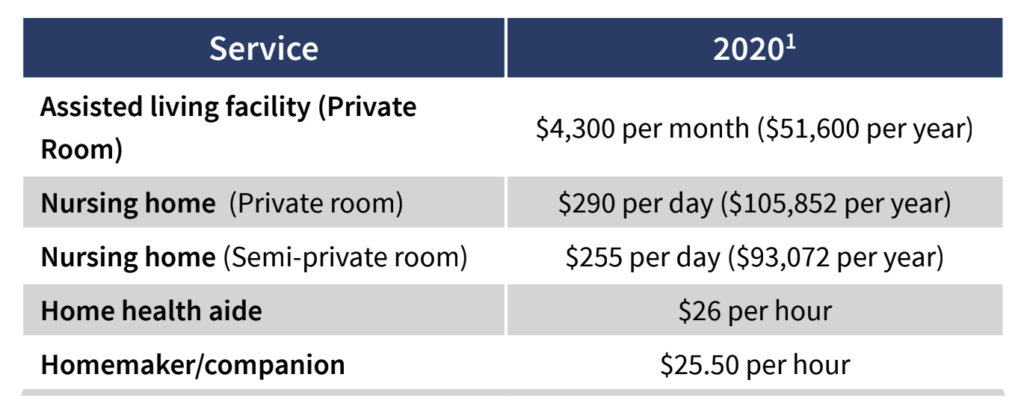

Much long-term care is paid for from personal resources:

Long-term care that is paid for by government comes from two primary sources:

In the past, some individuals have attempted to artificially qualify themselves for Medicaid by gifting or otherwise disposing of assets for less than fair market value. Sometimes known as “Medicaid spend-down”, this strategy has been the subject of legislation such as the Omnibus Budget Reconciliation Act of 1993 (OBRA ’93). Among other restrictions, OBRA ’93 provided that gifts of assets within 36 months (60 months for certain trusts) before applying for Medicaid could delay benefit eligibility.

The Deficit Reduction Act of 2005 (DRA) further tightened the requirements to qualify for Medicaid by extending the “look-back” period for all gifts from 36 to 60 months. Under this law, the beginning of the ineligibility (or penalty) period was generally changed to the later of: (1) the date of the gift; or, (2) the date the individual would otherwise have qualified to receive Medicaid benefits. This legislation also clarified certain “spousal impoverishment” rules,

while making it more difficult to use certain types of annuities as a means of transferring assets for less than fair market value.

1Source: U.S. Census Bureau, 2019 American Community Survey 1-Year Estimates, Sex by Age by Disability Status for the Civilian noninstitutionalized population, male and female, Table B18101.

2See “Long-Term Services and Supports for Older Americans: Risks and Financing, 2020,” Table 1. U.S Department of Health and Human Services, Office of Behavioral Health, Disability, and Aging Policy. January 2021.

Getting started is easy! Simply fill out the form below and set up a meeting with one of our experienced team members. In this introductory call, we’ll discuss your financial goals and go over the materials we need from you in order to move forward.

Ausdal Financial Partners, Inc., Registered Investment Advisor, is registered with the SEC

Click here to download the Ausdal Client Relationship Summary

![]()

Copyright © 2024. Cornerstone Financial Partners & Associates, LLC.

"*" indicates required fields