Many people believe that their biggest asset is their home. For most of us, our biggest asset is

the ability to work and earn an income. Not being able to work – due to a job loss or a

disability having taken away the ability to work – is often financially devastating.

Everyone who works for a living is familiar with what can happen if they lose their job. On the

other hand, the possibility of a serious disability is a risk few seem to consider. How likely is it

that you will become seriously disabled? According to one study, 30% of all Americans

between the ages of 35 and 65 suffered a disability lasting at least 90 days.1 The risk is real. The question is, “What to do about it?”

A few individuals do manage to qualify for disability benefits from Social Security. However, the Social Security definition of “disability” is so strict that, in 2019, only 36.9% of initial claims for Social Security disability benefits were accepted.2

Obviously, something else beyond Social Security is needed.

Many employers will provide – or make available – disability insurance on a group basis.

However, even those who are covered by a group policy can still be at substantial risk.

Employer-sponsored disability policies seldom replace more than 60% of your monthly

salary. Further, many policies have a monthly maximum benefit that may be far less than

what some people earn. Income taxes can also be an issue; if the employer is paying the full

cost of the coverage, and not including it in the employee’s income, disability benefits are

fully taxable. If an employee pays for disability insurance with after-tax dollars, the benefits

are received free of income tax.3

If group coverage is not available, the solution may be individual disability income insurance. Although individual policies can cost more, as long as you pay the premiums with after-tax dollars, the benefits are not taxable. Plus, an individual policy allows you to tailor its terms to fit your own needs. When shopping for an individual disability policy, consider the following:

● Company strength: You need to know if the company is financially sound.

● Definition of disability: Look for a policy that defines disability in the broadest terms possible. Some policies will permit you to work in a different occupation and still

collect disability benefits.

● Elimination period: How long must you wait before disability payments begin?

● Benefit period: How long will you need coverage? Both short-term and long-term

disability benefits are available.

● Inflation protection: Try to find a policy that adjusts benefits for inflation.

While most Americans insure their lives and physical possessions such as their homes, cars,

etc., many overlook the need to protect their most valuable asset – the ability to earn an

income.

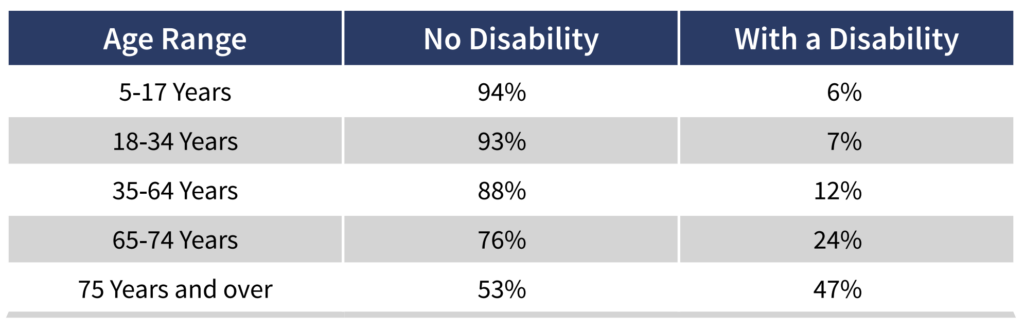

How likely is it that someone will become disabled? The table below, developed using data

collected by the federal government, shows the number of working-age Americans who have

a disability that affects their daily lives.